The emerging manager paradox

By the time the data arrives, the decision about your future has already been made

The advice given to first-time fund managers is consistent and mostly correct. Build relationships early. Be authentic. Add value to founders before you need anything in return. Stay close to the market. Be patient. None of that is wrong. But it sits slightly to the side of the actual structural challenge, which is not simply that raising a first institutional fund is hard, it is that the feedback loop on whether you are good at the job closes too late to help you when you need it most.

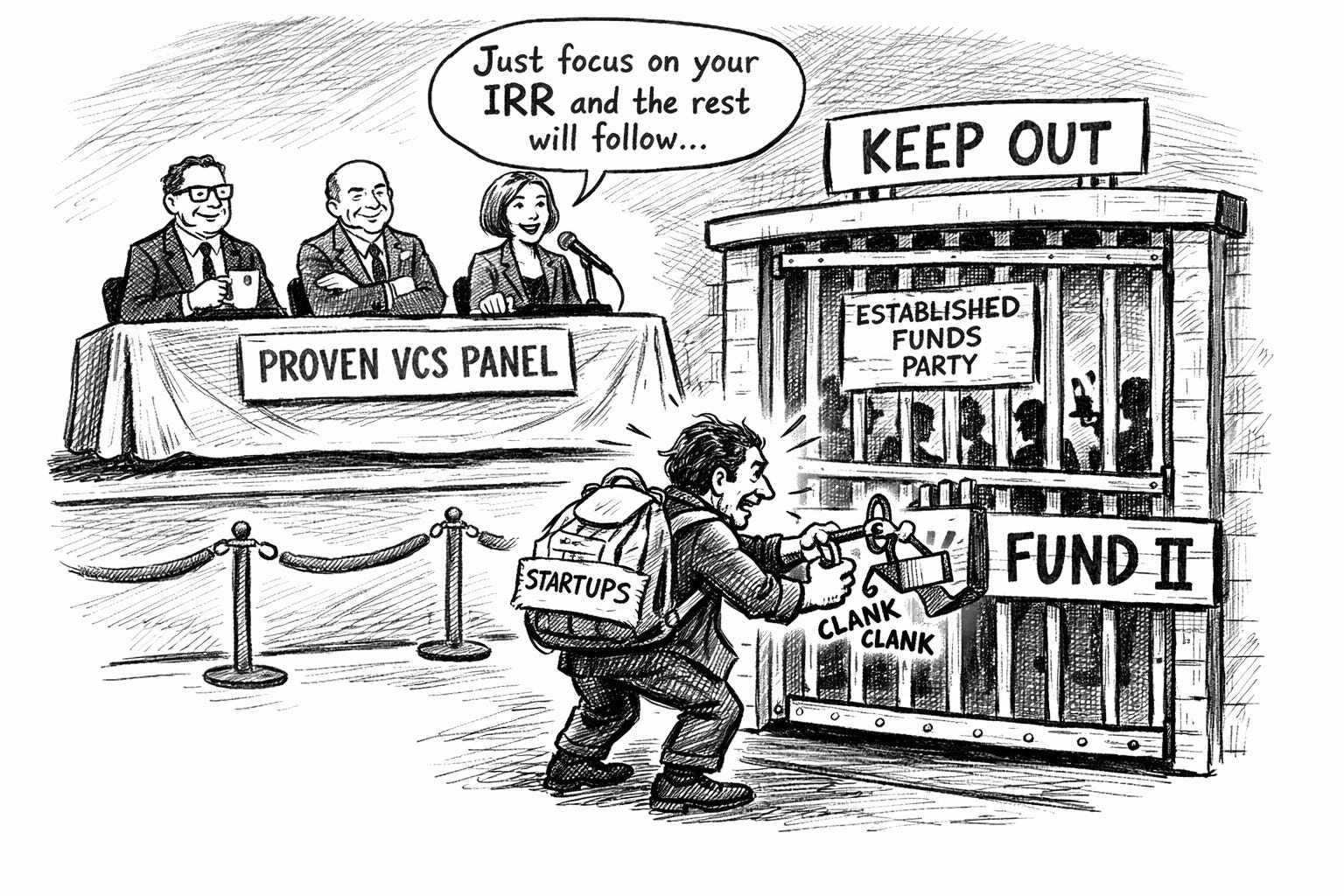

That matters because the point of maximum exposure for a first-time manager is usually not the beginning of Fund I, but the period in which Fund II has to be raised while Fund I is still too young to say much with confidence. In venture, meaningful performance dispersion takes time to become visible. The eventual distance between top-quartile and median outcomes is real, but in the early years the data is immature, marks are still soft, exits are rare, and even strong portfolios can look fairly ordinary from the outside. A manager building something genuinely exceptional and one who is not may look, from the outside, nearly identical. By the time the difference becomes obvious, the decision about whether that manager gets to keep going has often already been shaped.

There is an irony here that I find hard to ignore. Venture as an asset class is built on the idea that potential can be funded before proof. Founders raise on vision all the time. Investors routinely underwrite teams, markets, and products long before outcomes are certain. But the same ecosystem often becomes far more conservative when the object being underwritten is not the company, but the manager. Founders are allowed to be legible through possibility. GPs are often asked to be legible through evidence that, by the nature of the game, matures too slowly to be available when it is most needed. That mismatch is not going away. It is not a temporary market glitch. It is a structural feature of how venture fund formation works.

That is the trap, and also the thing most emerging managers are not told clearly enough. The system appears to reward performance, but in the period that matters most for survival, it often rewards something adjacent to performance: the ability to create credible conviction in advance of conclusive proof. That is not the same skill as investing well, though the two are obviously related. It is the ability to help LPs see why your strategy should work before time has done the job for you. It is the ability to make your edge legible while it is still early enough for someone else to act on it.

None of this is irrational. In fact, from the LP side, it is probably the only sensible way the system can work. LPs have their own constraints, and those constraints are not abstract. They have pacing needs, internal reporting lines, investment committees, portfolio construction targets, reputational considerations, and, perhaps most importantly, career risk. Backing a first-time manager whose fund is still too young to show clean separation from the pack is very different from backing an established franchise with a long and legible record. Even if the actual underlying risk is not always lower, it is much easier to explain, much easier to defend internally, and much less likely to look reckless in hindsight. LPs cannot wait for perfect evidence because by the time it arrives, the allocation window is gone. So they do what investors usually do under conditions of delayed feedback: they substitute proxies for proof.

That substitution is where the real selection mechanism lies. Emerging managers are told, implicitly or explicitly, that the market will eventually notice if they just keep doing good work. Sometimes it does. But “eventually” is doing far too much work in that sentence. A first-time GP does not have the luxury of waiting for eventual recognition if the next fund has to be raised on a timeline that sits several years ahead of mature fund-level evidence. In practice, the question is not only whether the portfolio will become good, but whether there is already enough reason for someone to believe it will become good before the proof becomes undeniable. And that belief is rarely built off IRR tables alone.

What tends to matter instead is whether an LP can point to something real and forward-looking that anchors conviction. Sometimes that is a differentiated sourcing engine. Sometimes it is a clear pattern of access to rounds that others struggle to get into. Sometimes it is simply repeated evidence of unusually strong judgment in conditions where judgment is still all anyone really has. But sometimes it is something harder to name — a personal story that explains not just why the manager started the fund, but why they are unusually suited to this particular corner of the market.

Mine starts when I was in my early teens. My brother went blind. I won’t pretend I fully understood what that meant at the time, but one thing became almost instinctive: I started showing him the way. Physically at first. Then in every other sense. And somewhere in that process, something wired itself into how I think. When I sit across from a founder today, the first question that forms in my head is not about the market or the model. It is: what’s holding them back? What’s the blind spot they cannot see? Who in my network could change something for them right now? That reflex did not come from a course or a framework. It came from years of living with someone who needed a different kind of seeing.

The second thing my brother’s blindness gave me is harder to say out loud. My parents had a lot on their mind. Understandably. I have come to understand — after enough conversations with people who know how these things work — that I may not always have felt seen enough during those years. What that produced in me was a drive to do more, to be more, to make it impossible to be overlooked. That chip is still there. I do not know many people who operate with the same sense of urgency I bring every day. It is a genuine advantage. It is also a difficult thing to live with — wins are hard to enjoy because the next thing is already pulling at you.

I say this not to explain myself but because it directly explains what we do at Golden Egg Check Capital. The fund is built around a simple idea: that the most important thing we can do for a founder is help them see what they cannot see on their own, and connect them to exactly the person who can change their trajectory at exactly the right moment. That is not a strategy I chose because it sounded compelling in a deck. It is what I have been doing, in one form or another, my entire life.

That is also the kind of story an LP can carry into committee. This is why so much of the conventional advice to emerging managers, while directionally correct, remains incomplete. It tends to treat relationship-building, portfolio construction, and performance as if they exist in a neat sequence: first do the work, then the results come, then the market rewards you. But for a first-time manager, those things happen on overlapping clocks. You are building the portfolio at the same time as you are building the interpretive frame through which others will understand it before it is fully formed. You are not only investing in companies. You are also, whether you like it or not, building the case for your own existence as a manager in a market that is predisposed to skepticism and working with incomplete information.

Seen that way, Fund I is not just a portfolio-building exercise. It is also a proof-of-concept for a GP market fit story — a coherent and truthful account of why this manager should exist, why this strategy makes sense, and why now is the moment to back it even though the data is not yet fully developed. The best versions of that story are not invented. They are discovered through the work itself. But they still need to be articulated. If they remain trapped inside the GP’s own head, or scattered across a hundred half-visible signals, they are not much use to an LP trying to take a defensible decision into committee.

The practical implication is uncomfortable, but also clarifying. If you spend the early years of Fund I quietly trying to optimize the portfolio while assuming the results will eventually speak for themselves, you are solving the right problem in the wrong register. Of course the portfolio matters — it matters most in the long run, and nothing real can be built without it. But in the medium-term window that determines whether you get the chance to keep compounding, performance alone is rarely enough because it is still too early, too noisy, and too easy to discount. The job is therefore dual from the start. You have to invest well, and you have to make the reasons your investing should work visible enough, early enough, and clearly enough that other people can carry that conviction before the data becomes decisive.

Legibility is part of the work. Every LP update, every portfolio reflection, every pattern you can make visible before it becomes obvious in the returns — all of it contributes to how belief gets built before proof arrives. The managers who understand this early are not waiting to be discovered. They are doing the slower, harder work of making their edge understandable while the proof is still in formation.

By the time Fund I can speak loudly enough for everyone to hear, the decision about whether you get to keep going has usually already been made. The feedback loop arrives after the damage is done.Thanks for reading More Ventures! Subscribe for free to receive new posts and support my work.

Multiple capital’s data has shown quite the opposite. Fund II can be raised purely on the premise that fund I’s raise was a success. It gets tricky where investors look at Fund III, then performance really counts. Thoughts?